.webp)

How Fintechs Handle GDPR Compliance

GDPR compliance is a must for fintechs handling sensitive financial and personal data. Non-compliance risks hefty fines (up to €20M or 4% of global revenue), reputational damage, and operational challenges. Here's what fintechs face and how they manage GDPR requirements:

- Data Complexity: Fintechs deal with scattered data across APIs and third-party tools, making tracking and documenting data flows difficult.

- Legal Basis & Consent: Processing activities like credit scoring or biometric authentication require specific legal grounds and explicit consent.

- Retention vs. Deletion: GDPR’s data minimization rules often conflict with financial regulations requiring long-term data retention.

- Cross-Border Transfers: Serving EU residents means navigating strict rules for transferring data internationally.

- Security & Breach Response: Breach notifications must happen within 72 hours, adding pressure to already complex cybersecurity efforts.

Fintechs address these challenges with structured solutions, including detailed data inventories, clear consent frameworks, retention policies, and robust vendor management. By embedding privacy into their systems and processes, fintechs can ensure compliance while safeguarding customer trust.

Startup Privacy Policies 🥷 What you need to know about GDPR, CCPA and beyond!

Main GDPR Challenges for Fintech Companies

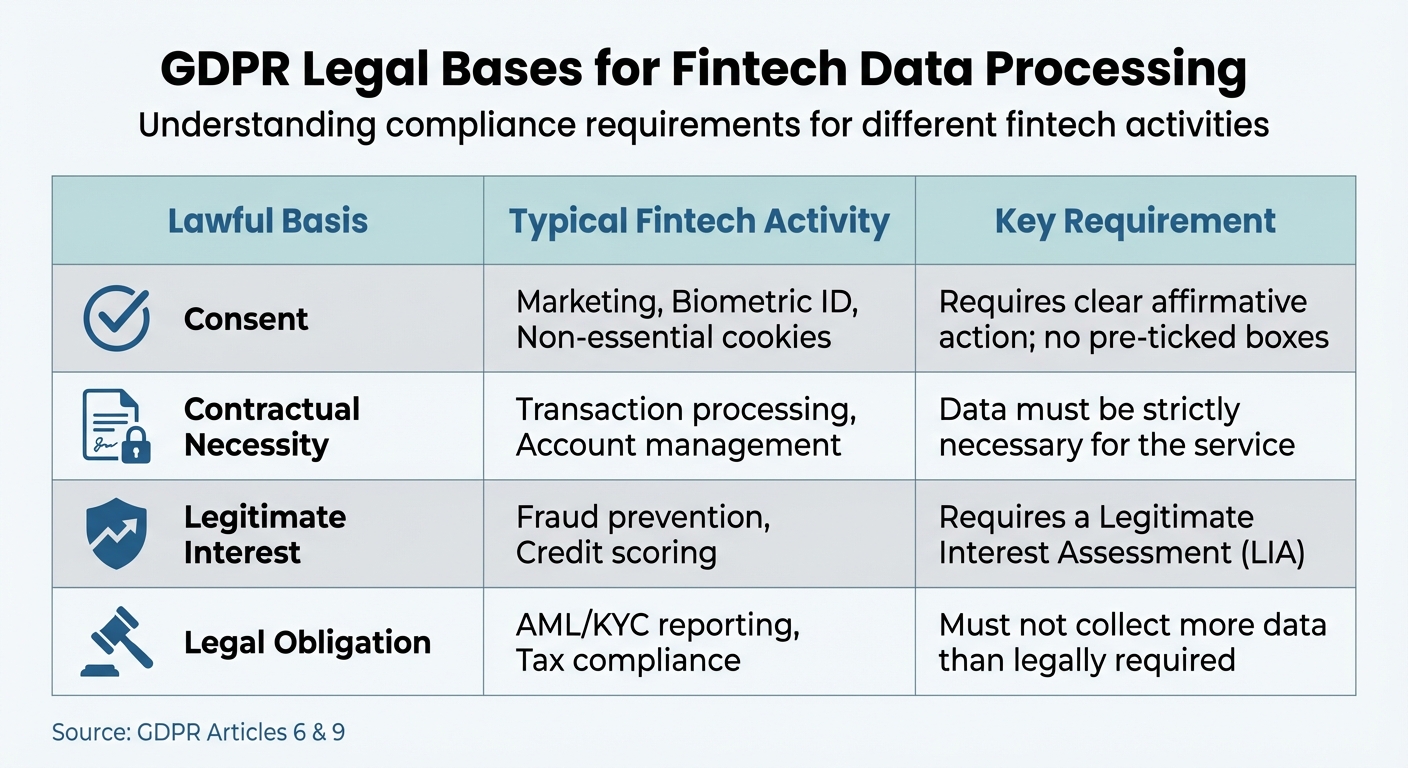

GDPR Legal Bases for Fintech Data Processing Activities

Tracking Data Across Multiple Systems

Fintech companies face a major hurdle: keeping track of data scattered across APIs and third-party tools. Unlike traditional banks with centralized systems, fintechs rely on modular architectures. These setups use APIs to connect customer data with external services like analytics, fraud detection, payment gateways, and credit bureaus. The result? Data flows that are often invisible and difficult to map or document.

Statistics paint a clear picture: 54% of financial leaders cite data silos as the biggest barrier to innovation, and 93% of fintech companies report challenges in meeting compliance regulations. High-growth fintechs often rely on complex stacks of third-party integrations, making it nearly impossible to maintain up-to-date Records of Processing Activities (RoPA).

"The architecture of fintech companies is modular; their services are real-time; and their third-party dependencies are extensive... resulting in a network of data flows that is not always fully visible to the business itself." - Paul Krasy, Data Protection Officer, Mentor Group

Under Article 30 of GDPR, organizations must document data processing activities in granular detail, linking purposes to specific data categories and individuals. For fintechs, which frequently roll out new features or integrations, keeping these records current is a constant challenge. The consequences are serious - Klarna Bank AB faced a €720,000 fine for failing to meet these compliance requirements.

Next, we’ll dive into how legal frameworks and consent protocols add another layer of complexity for fintech companies.

Managing Legal Basis, Consent, and Profiling

For fintechs, choosing the right legal basis for data processing is anything but straightforward. For example, biometric data requires explicit consent under GDPR, as it falls into special categories. Meanwhile, other activities rely on different legal bases: transaction processing on contractual necessity, fraud prevention on legitimate interest, and AML/KYC reporting on legal obligation.

Automated decision-making adds yet another layer of difficulty. Many fintech processes - credit scoring, fraud detection, and risk assessments - qualify as profiling under GDPR. With the EU AI Act now classifying these activities as "high-risk", fintechs must conduct stricter risk assessments and ensure human oversight. Systems that can’t clearly explain their decisions or lack human review risk regulatory scrutiny.

Here’s how typical fintech activities align with GDPR requirements:

| Lawful Basis | Typical Fintech Activity | Key Requirement |

|---|---|---|

| Consent | Marketing, Biometric ID, Non-essential cookies | Requires clear affirmative action; no pre-ticked boxes |

| Contractual Necessity | Transaction processing, Account management | Data must be strictly necessary for the service |

| Legitimate Interest | Fraud prevention, Credit scoring | Requires a Legitimate Interest Assessment (LIA) |

| Legal Obligation | AML/KYC reporting, Tax compliance | Must not collect more data than legally required |

The regulatory landscape becomes even trickier when financial retention rules clash with GDPR’s privacy requirements.

Balancing GDPR with Financial Retention Requirements

Fintech companies often find themselves caught between two conflicting rules: GDPR’s data minimization and deletion requirements versus financial regulations that mandate data retention. For instance, under EU KYC frameworks, fintechs must retain customer data for at least five years after the business relationship ends. But this creates problems when customers invoke their "right to be forgotten."

The solution? Retain only the legally mandated records - such as KYC documents - in secure archives, while deleting non-essential data once its purpose is fulfilled. Granular retention schedules that specify timelines for different data categories are far more effective than blanket policies.

When denying deletion requests, transparency is key. Fintechs must provide clear documentation explaining why certain data must be retained, citing specific financial regulations. Importantly, the lawful basis for retaining such data should be "compliance with a legal obligation", not consent, since consent can be withdrawn.

Managing Cross-Border Data Transfers

GDPR compliance doesn’t stop at borders. Any fintech serving EU residents must comply, regardless of where it operates. For U.S.-based fintechs, this creates immediate challenges with cloud infrastructure and vendor relationships.

Standard Contractual Clauses (SCCs) are the go-to mechanism for cross-border data transfers. However, after the Schrems II ruling, simply signing SCCs isn’t enough. Fintechs must also conduct Transfer Impact Assessments (TIAs) to evaluate third-country data protection. Often, this means implementing additional safeguards like end-to-end encryption or pseudonymization.

Vendor ecosystems make this even more complex. Fintechs typically depend on global providers for services like cloud hosting, AML/KYC screening, and credit scoring. Each integration requires a detailed Data Processing Agreement (DPA) and verification of the vendor’s data transfer safeguards. Non-EU fintechs must also appoint an EU-based representative to act as a contact point for data subjects and authorities.

These challenges highlight the need for robust security measures, which we’ll explore next.

Security and Breach Notification Requirements

Handling sensitive data is a core part of fintech operations, and the stakes are high. 72% of finance Chief Risk Officers rank cybersecurity as their top concern, and it’s easy to see why. Fintechs face stricter security expectations than most industries, and GDPR’s breach notification rules add further pressure.

Under GDPR, companies must notify authorities of data breaches within 72 hours. But fintechs also have to meet financial regulators’ incident reporting requirements. Coordinating these overlapping processes - while simultaneously investigating the breach and containing the damage - can be overwhelming.

The impact of a breach goes beyond fines. Traditional banks enjoy a consumer trust score of 7.6 out of 10, but fintechs lag behind at 5.8 out of 10. Security breaches and poor fraud handling are key reasons for this gap. A single incident doesn’t just bring regulatory penalties - it can also erode the trust fintechs rely on to compete with established banks.

These challenges set the stage for discussing practical GDPR solutions in the next section.

GDPR Solutions for Fintech Companies

The challenges discussed earlier are manageable with the right approach. Fintech companies can implement targeted strategies to meet GDPR requirements without stifling innovation. The goal is to create systems that are thorough yet adaptable - essentially, living documents that evolve alongside the business. These steps can help transform GDPR compliance into a structured and efficient process.

Building a Complete Data Inventory

Start by conducting a detailed audit to map out all personal data, including where it’s stored and how it flows through your systems. Businesses with 250 or more employees are legally required to maintain records of all processing activities. Smaller fintech companies must also document processing activities if they involve sensitive data or carry risks to individuals' rights.

To make this process effective, involve teams from IT, legal, and governance. Use simple, jargon-free questionnaires for departments like HR, Sales, and Customer Service to understand how they handle data. Follow up with interviews to confirm technical security measures and set appropriate retention periods.

Your Record of Processing Activities (RoPA) must include specific details as required by Article 30, such as processing purposes, data categories, recipients, retention schedules, and security measures. The Information Commissioner’s Office (ICO) emphasizes:

"A generic list of pieces of information with no meaningful links between them will not meet the UK GDPR's documentation requirements"

| Required Documentation Element | Description |

|---|---|

| Processing Purposes | Why the data is being used (e.g., AML/KYC, transaction processing). |

| Data Subject Categories | Types of individuals involved (e.g., customers, employees). |

| Personal Data Categories | Types of data collected (e.g., contact details, financial records). |

| Recipient Categories | Who the data is shared with (e.g., cloud providers, credit bureaus). |

| Retention Schedules | Timeframes for keeping data before deletion. |

| Security Measures | Protections like encryption and access controls. |

Treat your data inventory as a dynamic document, regularly updating it to reflect changes in data usage. Using specialized software can simplify updates and make it easier to locate data when responding to user requests.

Creating Legal Basis and Consent Frameworks

Choosing the correct legal basis for processing personal data is not just a formality - it’s a critical decision that must be documented and defensible. Article 5 of the GDPR states:

"The controller shall be responsible for, and be able to demonstrate compliance with, paragraph 1 ('accountability')"

For consent-based processing, ensure all mechanisms require active, positive opt-ins. Pre-ticked boxes or any form of default consent are not allowed. Consent requests should stand out and be separate from other terms of service. The ICO advises:

"Consent requests should be clear and specific (not a pre-condition of signing up to a service)"

If relying on legitimate interests, such as fraud prevention, fintechs must conduct a three-step Legitimate Interest Assessment: identify the interest, demonstrate the necessity of processing, and balance it against individual rights. Processing sensitive data like biometrics requires an additional lawful basis under Article 9.

| Requirement | Consent Criteria | Legitimate Interest Criteria |

|---|---|---|

| Action | Positive opt-in (no pre-ticked boxes) | Three-part balancing test (LIA) |

| Documentation | Record of what, when, and how consent was given | Documented assessment of necessity and impact |

| Withdrawal | Must be as easy to withdraw as it was to give | Opt-out options where possible |

| Specificity | Clear and granular for each purpose | Tied directly to the identified interest |

Automate processes to review and refresh consent periodically, especially when processing purposes or customer relationships change. Ensure your RoPA links each processing purpose to its legal basis, data categories, and retention schedules.

Setting Up Retention and Deletion Policies

Balancing GDPR’s "right to be forgotten" with financial record-keeping obligations requires clear retention schedules. For example, under the EU’s KYC framework (Directive (EU) 2015/849), fintechs must retain customer data for at least five years after the business relationship ends. However, not all data needs to be kept indefinitely.

Distinguish between data that must be retained for compliance, such as KYC documents, and data that can be erased, like marketing profiles or non-essential biometric information. Delete non-essential data promptly while securely archiving mandatory records.

Document retention periods in your RoPA as part of your legal obligations. The ICO highlights:

"The record of your processing activities needs to reflect these differences. A generic list of pieces of information with no meaningful links between them will not meet the UK GDPR's documentation requirements"

Automate deletion schedules to ensure compliance and simplify updates. If you cannot fully honor a deletion request due to legal requirements, explain this clearly in your privacy policy. Always verify the identity of individuals before processing deletion requests.

| Data Category | Typical Lawful Basis | Retention Driver |

|---|---|---|

| KYC/AML Documents | Legal Obligation | Anti-Money Laundering Directives (e.g., 5-year minimum) |

| Transaction Records | Performance of Contract / Legal Obligation | Financial record-keeping regulations |

| Biometric Data | Explicit Consent | Used for authentication; deletable if not legally required |

| Marketing Data | Consent / Legitimate Interest | Deletable upon request |

Responses to data subject requests, including deletion requests, must typically be provided within one month, with possible extensions for complex cases.

Managing Vendors for GDPR Compliance

Your GDPR compliance is only as strong as your weakest vendor. Any third-party service, from cloud hosting to KYC screening, must have a Data Processing Agreement (DPA) that outlines responsibilities, security measures, and breach protocols.

Before onboarding a vendor, assess their data protection policies, security certifications, and compliance track record. Maintain a vendor registry that documents what data is shared, the legal basis for sharing it, and the safeguards in place. Remember, GDPR violations related to vendor obligations can result in fines of up to €10 million or 2% of global revenue.

Vendor compliance isn’t a one-time task. Regularly review their security practices, conduct audits when necessary, and establish clear communication channels for incident reporting. Update DPAs whenever vendors change their services or processing activities.

sbb-itb-5f36581

Technical and Operational Controls for GDPR

Protecting Sensitive Data

Fintech companies need to safeguard sensitive data with strong measures like AES-256 encryption and TLS 1.3 for data in transit. The Information Commissioner's Office (ICO) has emphasized the importance of encryption, stating:

"considered encryption to be an appropriate technical measure given its widespread availability and relatively low cost of implementation"

Access to sensitive data should follow the principle of least privilege, requiring multi-factor authentication (MFA) - a combination of a password and either a token or biometric verification. Access rights should be updated regularly as roles evolve.

System resilience is equally important. Implement a "3-2-1" backup plan - three copies of data, stored on two different devices, with one copy kept off-site. Regularly test disaster recovery plans to ensure quick restoration of data after an incident. As the Federal Trade Commission warns:

"a financial institution's information security program is only as effective as its least vigilant staff member"

To strengthen defenses, combine technical controls with ongoing security training for employees.

Regular vulnerability scans and penetration tests, monitoring system logs for unauthorized activity, and securely deleting data that has reached the end of its retention period are all proactive measures. These steps form the backbone of a strong GDPR security framework, ensuring readiness to handle data subject requests effectively.

Handling Data Subject Rights Requests

Technical controls alone aren't enough - well-organized operational workflows are crucial for managing individual data rights. Fintechs typically have one month to respond to data subject rights requests, though this can be extended by two months for complex cases. The response timeline begins only after verifying the requester's identity, a critical step when dealing with sensitive financial information.

Establishing a clear intake process ensures that customer support teams can quickly identify and escalate these requests, whether they arrive via email, phone, or social media. If a customer asks for "all my data", you can pause the response clock by requesting clarification on what specific information they need. This approach avoids unnecessary searches across all systems.

Tools that enable system-wide searches can significantly speed up the process. Your Record of Processing Activities (RoPA) serves as a guide to locate various data types, simplifying responses. When fulfilling access requests, provide the data in commonly used formats like CSV or JSON.

If legal obligations - such as retaining Know Your Customer (KYC) data for anti-money laundering (AML) compliance - prevent you from taking certain actions, document these limitations and explain them clearly to the individual. Additionally, inform individuals of their right to file a complaint with a supervisory authority if their request is denied. Keeping detailed records of all requests and responses not only ensures compliance but also provides an audit trail for future reference.

Using Reform for GDPR-Compliant Data Collection

Specialized tools like Reform can streamline GDPR-compliant data collection. Design forms to capture only the necessary information, reducing the burden of processing excess data. Reform's no-code, conversion-focused form builder allows fintechs to create forms tailored for tasks like KYC verification, account setup, or managing privacy preferences.

Use multi-step forms with conditional routing to collect essential details first, such as contact information for contractual purposes, and then request explicit consent for marketing. This minimizes unnecessary data collection.

Reform also offers consent management features to record what users agreed to, when they agreed, and how consent was obtained. This aligns with GDPR's accountability requirements. Configure forms for clear opt-in consent without pre-selected options, ensuring explicit agreement. Self-service forms allow users to update preferences or withdraw consent, with changes automatically processed and an audit trail maintained.

Integration features let data flow directly into your CRM or compliance systems, categorized and tagged for retention. This reduces manual data entry errors and simplifies responses to data subject requests. Additional features like email validation and spam prevention help maintain data quality, while custom CSS and JavaScript support allows fintechs to add extra security without compromising the user experience.

Future Trends in Fintech GDPR Compliance

Stricter Enforcement and Regulator Coordination

GDPR enforcement has become tightly interwoven with financial regulations, placing fintech companies under dual scrutiny. While data protection authorities focus on GDPR compliance, financial regulators such as the FCA or BaFin oversee market conduct and anti-money laundering practices. A data breach today doesn’t just trigger GDPR-related investigations - it often opens the door to broader operational reviews.

The European Data Protection Board is stepping up efforts to coordinate enforcement across national authorities, especially for fintechs operating in multiple EU countries. This harmonized approach means penalties are becoming stricter and more consistent. Privacy is no longer just a box to check - it’s now a fundamental part of operational requirements. Financial supervisors increasingly integrate privacy concerns into their overall assessments, making GDPR compliance an essential part of product development from day one.

This growing regulatory overlap is also extending into new technologies, presenting fresh challenges for fintechs.

How GDPR Intersects with AI and Financial Regulations

As regulatory enforcement tightens, fintechs must grapple with the challenges posed by AI. The use of AI in financial services - whether for credit scoring or fraud detection - requires fintechs to establish a valid legal basis under GDPR Article 6 for processing personal data in machine learning models. Repurposing data for AI training adds another layer of legal complexity.

Generative AI introduces even more complications, particularly around data subject rights. For example, in March 2023, Italy’s Data Protection Authority temporarily banned ChatGPT over concerns about mass data collection without a valid legal basis and the system’s tendency to produce inaccurate information about individuals. These so-called AI "hallucinations" conflict directly with GDPR’s accuracy principle. Non-compliance with both GDPR and the EU AI Act can lead to severe penalties - up to €30 million or 6% of total global annual turnover.

Biometric data presents additional hurdles. Technologies like facial recognition and fingerprint authentication require explicit consent under GDPR, as well as robust security measures to handle this "special category" of data.

"Data protection should not be an afterthought but an integral component of the development process." – Information Security Institute

Building Flexible Compliance Programs

With regulatory demands evolving and AI challenges on the rise, fintechs need compliance programs that can adapt over time. Designing flexible systems is key. Modular architectures, for instance, allow fintechs to adjust to region-specific laws - like India’s DPDP or Brazil’s LGPD - without overhauling their entire infrastructure. This adaptability is increasingly seen as a competitive edge:

"The ability to comply with regulatory requirements has become a key source of competitive advantage for financial institutions." – Boston Consulting Group

Automated data reconciliation frameworks can help maintain traceability across fragmented systems, enabling fintechs to respond quickly to regulator requests. Regular breach response drills ensure readiness to meet GDPR’s strict 72-hour notification requirement. Aligning Data Protection Impact Assessments with AI Act risk management is also critical for high-risk technologies. Additionally, appointing specialized oversight roles - like a Data Protection Officer or an AI Ethics Officer - can help address the ethical and legal complexities of emerging technologies.

Real-time monitoring is becoming the norm in financial transactions. Instead of relying solely on periodic audits, many fintechs are adopting continuous monitoring systems that can flag compliance issues as they arise. This proactive approach, combined with modular frameworks and automated reconciliation, equips fintechs to navigate an increasingly complex regulatory environment with greater agility.

Conclusion

Meeting GDPR requirements is more than just a legal obligation - it's a way for businesses to build trust and gain an edge in the market. However, achieving compliance comes with its own set of hurdles, such as managing fragmented data tracking, balancing erasure rights with mandatory five-year KYC retention, navigating cross-border data transfers, and adhering to the 72-hour breach notification rule. To tackle these challenges effectively, fintechs need a clear and actionable strategy.

One critical step is embedding privacy-by-design into every product and process. This involves maintaining thorough Records of Processing Activities, conducting Data Protection Impact Assessments for high-risk activities like biometric authentication, and securing strong Data Processing Agreements with all vendors. As Kevin Yun of ComplyDog explains:

"Compliance with the GDPR is not just a legal obligation for FinTech startups; it's a fundamental component of responsible data handling practices and a key factor in building trust with customers and stakeholders".

The stakes for non-compliance are high, with penalties reaching up to $20 million or 4% of global turnover. But beyond avoiding fines, accountability can offer a competitive edge. Boston Consulting Group highlights this shift:

"the ability to comply with regulatory requirements has become a key source of competitive advantage for financial institutions".

As technologies like AI and biometric authentication continue to evolve, fintechs must stay flexible. Tools like automated workflows for handling data subject requests, regular breach response simulations, and modular compliance systems enable businesses to adapt to new regulations without overhauling their operations. By combining strong technical safeguards, well-defined legal frameworks, and efficient vendor management, fintechs can turn regulatory demands into opportunities for growth.

Ultimately, innovation grounded in privacy-by-design doesn't just help meet compliance - it sets fintechs apart in a crowded market. Those that see GDPR as a chance to innovate will not only protect their customers but also position themselves for success in an increasingly regulated industry.

FAQs

How do fintech companies track data across systems to stay GDPR-compliant?

Fintech companies tackle GDPR compliance by starting with a detailed data-mapping audit. This process pinpoints how personal data moves through their systems, giving them a clear picture of their data flow.

To streamline this, many adopt a centralized data pipeline or integration layer. This setup automatically syncs and logs personal data, ensuring they maintain an accurate and current record of all processing activities.

By doing so, they achieve greater transparency, improve data tracking accuracy, and make compliance reporting much more straightforward - all essential for meeting GDPR standards.

How do fintech companies manage GDPR's data deletion rules alongside financial record-keeping laws?

Fintech companies face the challenge of balancing GDPR's right to erasure with financial record-keeping laws, and they do so by meticulously organizing their data flows. They classify records based on legal retention requirements, identifying which data must be kept for compliance with laws like anti-money laundering or tax regulations and which can be deleted upon request. Many fintechs use automated systems to manage retention schedules, ensuring that data is promptly deleted once legal obligations are fulfilled.

When conflicts arise, such as U.S. financial laws mandating long-term data retention, fintechs often lean on GDPR exemptions like the "legal obligation" basis. To address privacy concerns while staying compliant, they frequently apply pseudonymization or anonymization techniques. These methods strip personal identifiers from the data, allowing it to remain usable for audits without compromising individual privacy.

To further streamline compliance, fintechs incorporate "legal hold" tools into their data management systems. These tools ensure that deletion processes pause for any ongoing regulatory needs. By combining precise data mapping, lawful retention practices, and automated workflows, fintech companies effectively navigate the complexities of GDPR and financial regulations.

How do fintech companies ensure GDPR compliance when using AI technologies?

Fintech companies are actively working to ensure their AI technologies meet GDPR standards. A key approach is embracing privacy-by-design principles, which means building data protection measures directly into AI systems from the ground up. This involves improving consent processes, maintaining high data quality, and setting up strong governance structures to manage AI operations responsibly.

Another major focus is on transparency and explainability. Fintechs are making sure users can clearly understand how their data is being used and that AI-driven decisions are both lawful and fair. To stay ahead of compliance challenges, many companies are also using real-time monitoring tools. These tools help identify potential risks, allowing businesses to remain accountable and steer clear of hefty penalties.

Related Blog Posts

Get new content delivered straight to your inbox

The Response

Updates on the Reform platform, insights on optimizing conversion rates, and tips to craft forms that convert.

Drive real results with form optimizations

Tested across hundreds of experiments, our strategies deliver a 215% lift in qualified leads for B2B and SaaS companies.